The following is a guest post and analysis from Shane Neagle, Editor In Chief fromThe Tokenist.

On June 13th, Charles Hoskinson, the co-founder of Ethereum (ETH) and founder of Cardano (ADA), made a bold proposition. In order to put Cardano on the decentralized finance (DeFi) map, the blockchain ecosystem should establish a sovereign wealth fund.

Specifically, to convert 5–10% of the ADA treasury (~$1.2 billion) into harder assets such as Bitcoin or tokenized dollars in the form of stablecoins. Let’s examine the implications of this proposal for Cardano and the wider crypto market.

The Point of a Sovereign Wealth Fund

Sovereign wealth funds are typically associated with governments. Case in point: oil-rich Norway has the Government Pension Fund Global (GPFG), from which the government draws an amount equal to ~20% of the nation’s budget. Although oil and gas production was the baseline for the fund’s growth, this sector now accounts for less than half of the fund’s total value.

Instead, the fund grows from stock exposure—around 9,000 companies across the world—alongside exposure to fixed income such as bonds (debt issued by governments), real estate, and renewable infrastructure. From 2019 to 2024, Norway’s sovereign wealth fund doubled in value, from $996 billion to nearly $2 trillion.

Therefore, GPFG consistently captures gains from broad market returns, but also from the government’s need to keep spending through debt. Hoskinson hopes to make similar gains through exposure to Bitcoin/stablecoins, and then use those proceeds to acquire more ADA, which would boost ADA’s price.

This strategy is sound for two reasons:

- First, it is a certainty that the U.S. government will spend beyond its means, which will further erode people’s purchasing power with USD. Already institutionalized through spot-traded ETFs, this means that Bitcoin will continue to serve as a wealth-safeguard asset due to its fixed scarcity and proof-of-work security. Likewise, outside of Bitcoin mining companies potentially erecting sell pressure, Bitcoin is not an asset concerned with earnings, unlike stocks.

- Second, exposure to stablecoins is exposure to USG’s sovereignty itself. Both Circle (USDC) and Tether (USDT) have massive exposure to U.S. Treasuries. While Tether is nearing $120 billion in U.S. Treasuries, delivering Q1 profit over $1 billion, Circle Reserve Fund has 49.64% in U.S. Treasury debt and 50.36% in U.S. Treasury repurchase agreements.

Owing to such exposure, these top two stablecoin companies are now significant generators of demand for U.S. debt. And as they earn yield, USG is happy because stablecoins extend financial hegemony into the digital sphere. Moreover, this keeps the yield on U.S. Treasuries at a manageable level.

The present U.S. Secretary of Commerce, Howard Lutnick, had already made this clear in April 2024, when he was the CEO of Cantor Fitzgerald:

“Dollar hegemony is fundamental to the United States of America. It matters to us, to our economy…That’s why I’m a fan of properly backed stablecoins. I’m a fan of Tether. I’m a fan of Circle.”

Cardano’s exposure to stablecoins would also be timely because it is the first blockchain asset likely to receive comprehensive regulation.

What About Cardano (ADA) Performance?

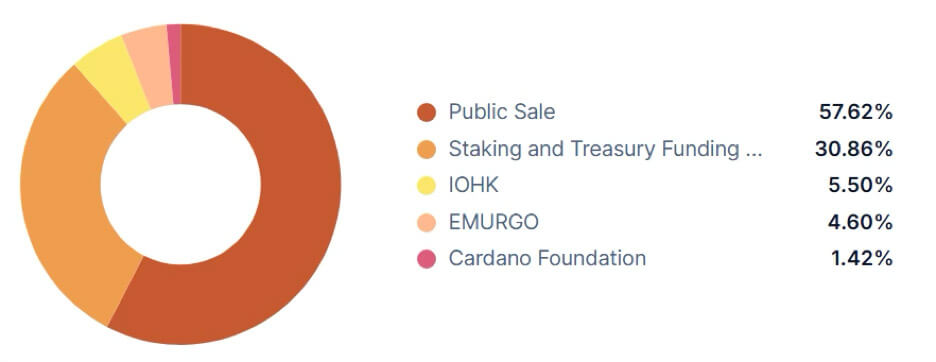

Year-to-date, ADA is down nearly 35% but up 56% over a one-year period. Out of its maximum supply of 45 billion ADA, Cardano has 35.36 billion ADA in circulation, leaving plenty of tokens yet to enter circulation and potentially drop ADA’s price if the demand is not there. Cardano’s annual inflation rate is ~2%, which is incidentally the Federal Reserve’s target inflation rate.

ADA’s treasury allocation is nearly 31%, from which 5–10% would be converted into either Bitcoin or stablecoins. As a proof-of-stake blockchain, Cardano gives 80% of staking rewards to validators, while 20% are reserved for the treasury.

Given Cardano’s relatively high inflation rate of 2% (Bitcoin has 0.82%), converting more ADA into Bitcoin/stablecoin would pose significant selling pressure that would depress ADA’s price. However, Hoskinson believes this could be mitigated.

Specifically, if 140 million ADA is converted into BTC/stablecoins, such purchases would be spread out over a week via over-the-counter (OTC) exchange desks utilizing a time-weighted average price (TWAP) strategy. TWAP relies on customized time-in-force settings to control execution timing and minimize market disruption.

Notably, Michael Saylor uses this strategy for Strategy’s BTC accumulation. After all, because MSTR stock price is a proxy exposure to Bitcoin, it is in Saylor’s interest to go under the radar during the order execution. Similarly, Hoskinson would have to maintain ADA’s average market price to avoid spooking the market.

Long-term, if gains from BTC and stablecoin exposure lead to repurchasing ADA—similar to stock buybacks—Hoskinson could gain the same benefit as Saylor does with MSTR stock, which regularly outperforms Bitcoin itself due to Saylor’s favorable access to credit markets.

What About Cardano’s Core Demand?

As Ethereum’s dissenting original co-founder, Hoskinson launched Cardano as a robust alternative that is more profit-oriented. To become a blockchain-based ecosystem for DeFi, Cardano first had to complete its smart contract functionality. This was made possible with the completion of the Goguen era, consisting of Allegra, Mary, and Alonzo hard forks in September 2021.

Still in the Basho scaling stage before the Voltaire governance era, Cardano’s blockchain performance is significantly behind the top 10 performers, headed by Solana. According to ChainSpect, Cardano is ranked 34th in real-time transactions per second (TPS) at 0.26 tx/s against its maximum theoretical TPS of 18.02 tx/s.

This gives the chain a finality of 2 minutes against Solana’s 12.8 seconds. Suffice it to say, until Basho is completed, in particular the Hydra layer-2 solution, this is not a competitive position. It is also not confidence-boosting that Cardano is three years older than Solana.

Combined with the fragmentation of the crypto market, and a devastating string of bankruptcies during 2022 culminating in the FTX collapse, Cardano holds only $267.5 million in its DeFi apps compared to $8.3 billion in Solana, or $62.7 billion locked in Ethereum’s dApps.

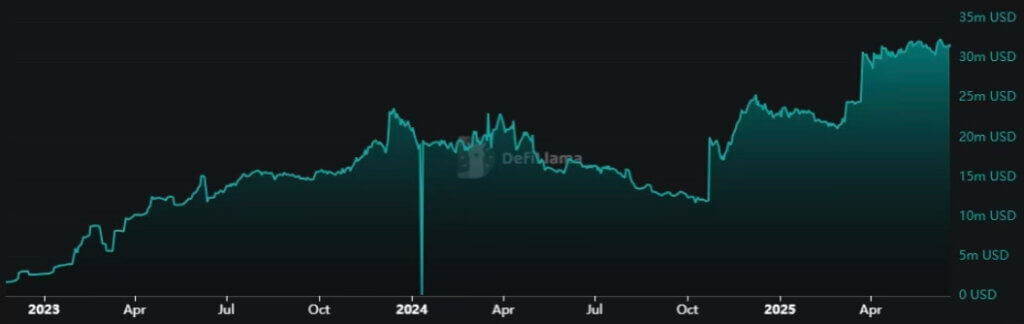

Moreover, stablecoins only account for $31.44 million in Cardano.

Considering the dwindling gains in the wider altcoin market, as more launched tokens dilute capital, it is now more important than ever to have a stablecoin price anchor. This would make lending and borrowing on dApps less risky with more predictable interest payments.

Likewise, stablecoins on decentralized exchanges (DEXes) offer less slippage and reduced impermanent loss, providing stable yield farming in the process. An inflow of stablecoin liquidity (~$100 million) would likely increase Cardano’s dApp activity. After all, it would be a much safer exposure than gambling on largely fraudulent memecoins.

Already, Cardano’s top dApp by unique active wallets (UAW) is a DEX aggregator called DexHunter, while borrowing and lending dApp Lenfi holds the most value at $11.62 million. Of course, these figures pale in comparison to dApp activity on the top 10 blockchains, which is why Hoskinson’s push is much needed.

The Bottom Line

In late May, the Ethereum Foundation borrowed $2 million in stablecoins from Aave with wrapped ETH (wETH) as the collateral. This dynamic, in which there was no need to sell ETH, points to a more mature DeFi ecosystem that Cardano is yet to approach.

Yet, to reach such maturity, Cardano has to start making bold moves. Allocating some portion of the ADA treasury into Bitcoin and stablecoins is a trajectory in the right direction. At a glance, it may seem that Hoskinson gives preference to BTC over ADA with this move, but it is a conflation of categories.

It is widely understood that Bitcoin acts as a store of value rather than a general-purpose smart contract blockchain like Cardano. Lastly, the current Trump administration clearly signaled that stablecoins will be a sufficient alternative to a cancelled CBDC. It is in this period that Cardano has to stimulate activity, without waiting on the completion of its scalability era.

The post Is Cardano’s plan to convert part of ADA treasury into Bitcoin a wise move? appeared first on CryptoSlate.